Section 409a Internal Revenue Code

Internal Revenue Code Section 409a Youtube

Https Www Ipbtax Com Media Publication 86 Code 20section 20409a 20hidden 20deferred 20compensation Pdf

Staying Compliant With Irc Section 409a Wimbush Associates Inc

Section 409a What Is New And Next Online Cle Course Lawline

Nonqualified Deferred Compensation Plans And Section 409a Plansponsor

Section 409a Top 10 Rules For Compliant Non Qualified Deferred Compensation

Notwithstanding section 885 d 1 of the american jobs creation act of 2004 pub.

Section 409a internal revenue code. 409a affects nonqualified retirement plans and other deferred compensation arrangements. Service recipients are generally employers but those who hire independent contractors are also service recipients. Notwithstanding section 885 d 1 of the american jobs creation act of 2004 subsection b of section 409a of the internal revenue code of 1986 shall take effect on january 1 2005.

Effective generally january 1 2005 congress set off a sea change in the tax treatment of nonqualified deferred compensation arrangements with the adoption of new section 409a of the internal revenue code. Executive employment and severance pay under section 409a of the internal revenue code. Internal revenue code 409a.

409a u s. Section 409a affects a broad array of compensation arrangements. Section 409a of the united states internal revenue code regulates nonqualified deferred compensation paid by a service recipient to a service provider by generally imposing a 20 excise tax when certain design or operational rules contained in the section are violated.

In 2004 the us congress passed the american jobs creation act creating section 409a of the internal revenue code section 409a in response to a perceived abuse of deferred compensation arrangements that were in the media spotlight in the wake of several significant corporate scandals at the time. Section 409a of the internal revenue code is a complex and often counterintuitive set of tax rules applicable to deferred compensation. 109 135 provided the following.

It created a new section 409a of the internal revenue code 409a and the code respectively. Code unannotated title 26. An internal revenue code section 409a primer by tony ling and galen mason1 the american jobs creation act of 2004 was signed into law on october 22 2004.

Irc Section 409a

Severance Arrangements And Code Section 409a Haynes And Boone Blogs Haynes And Boone Blogs

Guidance On Deferred Compensation Irc 409a And Irc Ppt Download

Irc Section 409a V Covid 19 The Nonqualified And Executive Compensation Clash And How Employers Can Navigate It

Irc 409a Overview 409a Valuations Explained Equityeffect

Http Www Buchalter Com Wp Content Uploads 2013 06 Client Alert 409a Pdf

Amazon Com Practical Guide To Code Section 409a 9780808022084 Michael Falk Books

Proposed Changes Clarifications And Additions To Deferred Compensation Agreements Under Irc Section 409a Sikich Llp

How To Fix Broken Legislation In The 409a Process Carta

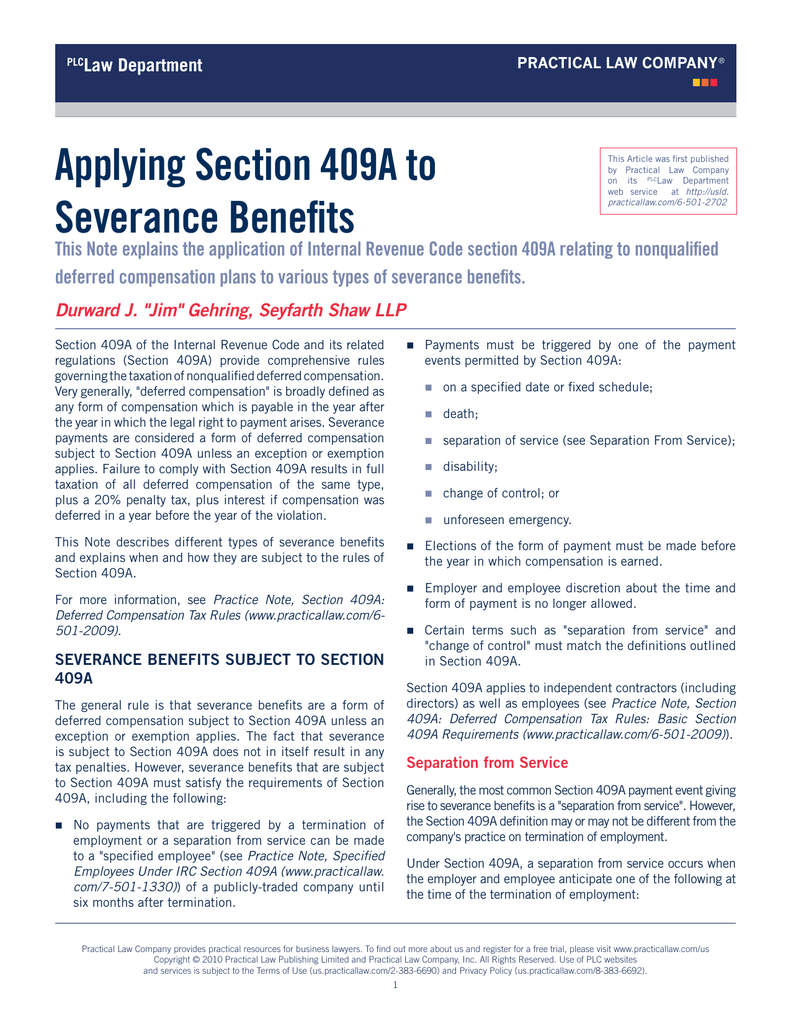

Applying Section 409a To Severance Benefits

Https Www Fenwick Com Fenwickdocuments Execu Comp 04 16 07 Pdf

What Is A 409a Valuation Report

Irs Code Section 409a And Its Impact On Stock Options Exit Promise