Section 1250 Property Examples

1231 1245 And 1250 Property Used In A Trade Or Business Investing Infographic Investment Quotes Investing

Excel Timesheet Calculator Template For 2020 Free Download Excel Tutorials Excel Excel Hacks

Http Media Straffordpub Com Products Calculating Depreciation Recapture Under Irc 1245 And 1250 Minimizing Tax Through Transaction Planning 2017 08 15 Presentation Pdf

Example Of Commercial Invoice Document Used For Import Export Global Trade Incodocs Import Exports Database Export Business Import Business Stock Market

Salary Format In Excel Free Download Google Search Payroll Template Resume Template Free Coupon Template

Types Of Triangles Printable Worksheet Worksheet Identifying Types Of Triangles Math Notebooks Printable Worksheets Fifth Grade Math

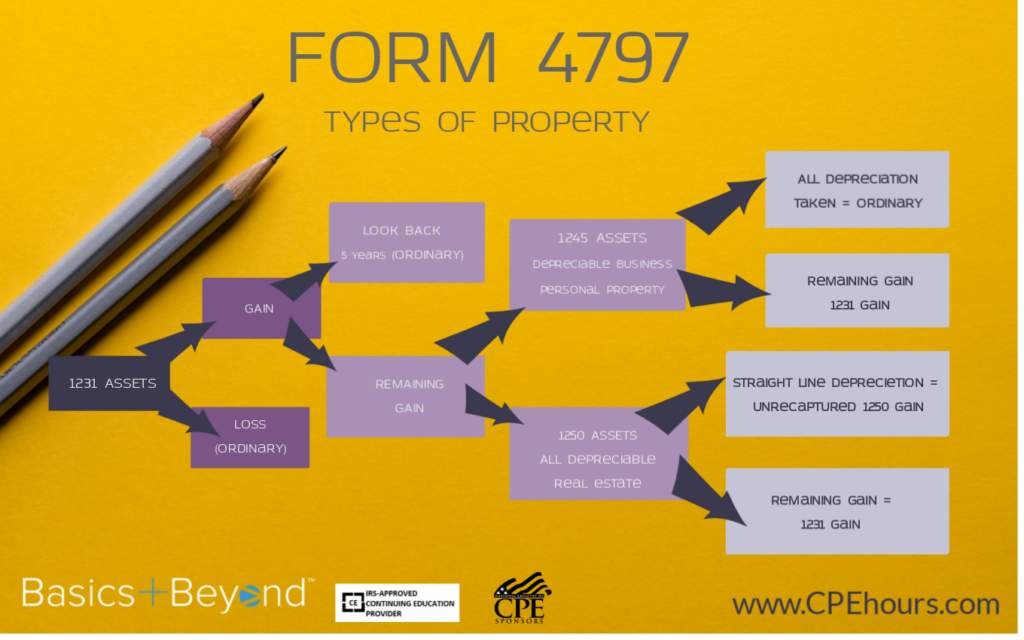

The internal revenue code includes multiple classifications for property.

Section 1250 property examples. Unrecaptured section 1250 gain only applies to depreciable real estate such as commercial real estate and residential rental properties. To observe a real world example of section 1250 in action imagine an investor buys an 800 000 real estate property with a 40 year useful life. 1250 propety is taxed similiarly to 1245 property with the recapture of depreciation.

Five years later employing the accelerated. 1250 property includes real estate and real property subject to depreciation that is and has not been section 1245 property. Learn about 1231 1245 1250 property and its treatment for gains and losses.

If a 100 000 asset is purchased and depreciation equals 50 000 upon sale of property the first 50 000 of gains are taxed at ordinary tax rates and any gain in excess of purchase price is taxed as a capital gain. Example of unrecaptured section 1250 gains if a property was initially purchased for 150 000 and the owner claims depreciation of 30 000 the adjusted cost basis for the property is considered.

How To Draft A Family And Medical Leave Guidelines For Leave Of Absence Download This Hr Leave Of Absence Policy Template Now Medical Leave Medical Guidelines

Samples Of Proposal Letters For Sponsorships In 2020 Sponsorship Proposal Sponsorship Package Event Sponsorship

:max_bytes(150000):strip_icc()/GettyImages-1174783581-020e7504020947dc979f864f2ebee096.jpg)

Section 1250 Definition

Sale Of Business Assets What You Need To Know About Form 4797 Basics Beyond

Gallery Of Life After Madrid Arhitektura D O O 17 Space Saving Kitchen Making Space Small Apartments

Pin By Aimee Fawn On Kabbalah Jewish Sephiroth Bible Study Notebook Bible Facts Inductive Bible Study

Https Www Calt Iastate Edu System Files Premium Video Files Powerpoint 20 20sale 20of 20business 20assets Pdf

German Essential Phrases In 2020 German Phrases Learning German Language Learning German Phrases

Pin De Irish Ultrafollowmyheart Em Sprechen Palavras Em Alemao Aprender Alemao Gramatica Alema

Pin On Reading

Wpf Chart Custom Tooltip Templates Example Scichart Wpf Charts Templates Custom Chart

Restaurant Specific Chart Of Accounts For Quickbooks Windows Desktop Chart Of Accounts Quickbooks Accounting

1231 1245 And 1250 Property Used In A Trade Or Business