Section 1231 Exchange

Pin On Holiday Printable A That Are Custom

/man-working-in-computer-1135595001-31f457ad7db84839938774cea99939e0.jpg)

Section 1231 Property

Pin On Tacky Holiday Sweaters

Https Farmoffice Osu Edu Sites Aglaw Files Site Library Taxpdf Ch 203 20form 204797 281 29 Pdf

Taxation Of Business Entities Ppt Download

Options To Reduce Tax On Sale Of Real Estate Used In A Business

Property deducted under the de minimis safe harbor for tangible property.

Section 1231 exchange. The term which gets its name from irs code section 1031 is. The term section 1231 loss means any recognized loss from a sale or exchange or conversion described in subparagraph a. 4 special rulesfor purposes of this subsection a in determining under this subsection whether gains exceed losses.

Section 1231 gains and losses. In real estate a 1031 exchange is a swap of one investment property for another that allows capital gains taxes to be deferred. If you will get back all or nearly all of your investment in the property by selling it rather than by using it up in your business it is property held mainly for sale to customers.

Section 1231 is the section of the internal revenue code that governs the tax treatment of gains and losses on the sale or exchange of real or depreciable property used in a trade or business and held over one year. Whether you sell one piece of section 1231 property or your entire business section 1231 rules apply. Like kind exchanges when you exchange real property used for business or held as an investment solely for other business or investment property that is the same type or like kind have long been permitted under the internal revenue code.

The present version of the internal revenue code has retained section 1231 with the provision now applying to both property lost in an involuntary conversion and to the sale or exchange of certain kinds of business use property. The term 1031 exchange is defined under section 1031 of the irs code. 1 to put it simply this strategy allows an investor to defer paying capital gains taxes on an investment property when it is sold as long another like kind property is purchased with the profit gained by the sale of the first property.

Section 1231 property is real or depreciable business property held for more than one year. Nonrecaptured section 1231 losses. Section 1231 property is a type of property defined by section 1231 of the u s.

Treatment as ordinary or capital. Section 1231 does not apply to a sale exchange or involuntary conversion of an unharvested crop if the taxpayer retains any right or option to reacquire the land the crop is on directly or indirectly other than a right customarily incident to a mortgage or other security transaction. Generally if you make a like kind exchange you are not required to recognize a gain or loss under internal revenue code section 1031.

Pin By Redwickerbasket On Burda Butterick Kwik Sew Advance In 2020 Sewing Patterns For Kids Sewing Patterns Kids Activity Books

Porcelain Santa Claus Head And Hands Dark Blue Eyes Round Dark Blue Eyes Male Doll Doll Parts

Pin Su Christmas Decorations

Pin On Nails

Like Kind Exchange

Pin On Beautiful Medical Id Bracelets For Diabetes Heart Disease Lymphedema Etc

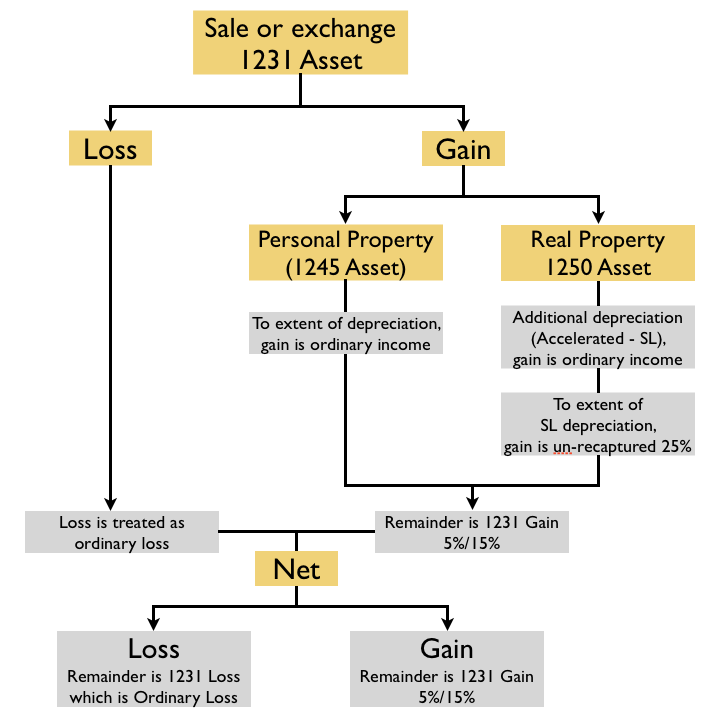

Flowchart Of Sale Or Exchange Of Property Section 1231 1245 And 1250 Assets Reg Notes Cpa Exam Club

Your Place To Buy And Sell All Things Handmade Male Doll Book Decor Old World

Metal Mobile Home Skirting Installation Lighthouseshoppe Com Deck Railing Design Modern Outdoor Patio Railing Design

Https Www Lw Com Thoughtleadership Basics Of Like Kind Exchanges Of Oil And Gas Properties

Https Www Calt Iastate Edu System Files Premium Video Files Powerpoint 20 20sale 20of 20business 20assets Pdf

Fab Events Sip Swap Shop The Style Medic Swap Party Swap Shop Shopping

/GettyImages-929595526-69ab1adce68740c3882d60964c12bea9.jpg)

What Is A Capital Asset