Section 121 Of The Internal Revenue Code

Planning Opportunities With The Sec 121 Partial Exclusion

3 12 10 Revenue Receipts Internal Revenue Service

25 6 1 Statute Of Limitations Processes And Procedures Internal Revenue Service

The Home Sale Gain Exclusion

A Trust Can Qualify For A Section 121 Deduction Pollock Firm

Sale Of Primary Residence Capital Gains Tax

This home sale gain exclusion lets you exclude i e not pay tax on up to 250 000 of gain on the sale of your primary residence if you are single or 500 000 of gain on the sale of your primary residence if you are married filing jointly with your spouse.

Section 121 of the internal revenue code. Section 121 of the internal revenue code of 1986 as amended by this section shall be applied without regard to subsection c 2 b thereof in the case of any sale or exchange of property during the 2 year period beginning on the date of the enactment of this act if the taxpayer held such property on the date of the enactment of this act and fails to meet the ownership and use requirements of subsection a thereof with respect to such property. Section 121 26 u s c 121 the internal revenue code section that addresses taxable income upon the sale of a principal residence an unmarried individual may exclude up to 250 000 of gain from income married persons filing joint returns may exclude up to 500 000 of gain the taxpayer must have owned and occupied the property for at least 2 of the prior 5 years and this exclusion can be used as frequently as every 2 years for many americans this ability to buy a home fix it up sell it in. Section 121 a generally provides with certain limitations and exceptions that gross income does not include gain from the sale or exchange of property if during the 5 year period ending on the date of the sale or exchange the taxpayer has owned and.

Internal revenue code 121. Findlaw codes are provided courtesy of thomson reuters westlaw the industry leading online legal research system. For more detailed codes research information including annotations and citations please visit westlaw.

1031 Exchange And Primary Residence Asset Preservation Inc

3 13 2 Bmf Account Numbers Internal Revenue Service

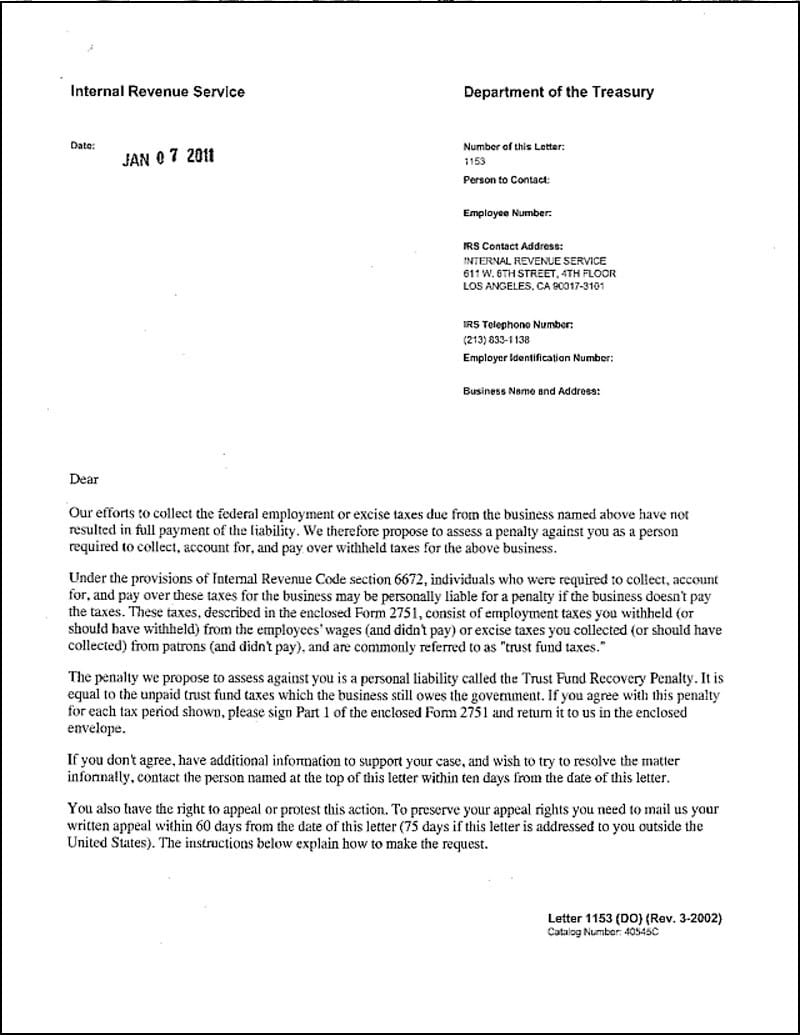

Irs Letter 1153 What It Means How To Respond Paladini Law

Selling Farmland Or A Ranch Irc Section 121 And Section 1031 Farmland Ranch Buying Property

Sec 163 Interest

National Internal Revenue Code Of 1997 Chan Robles Associates Law Firm

Https Www2 Illinois Gov Rev Research Publications Pubs Documents Pub 130 Pdf

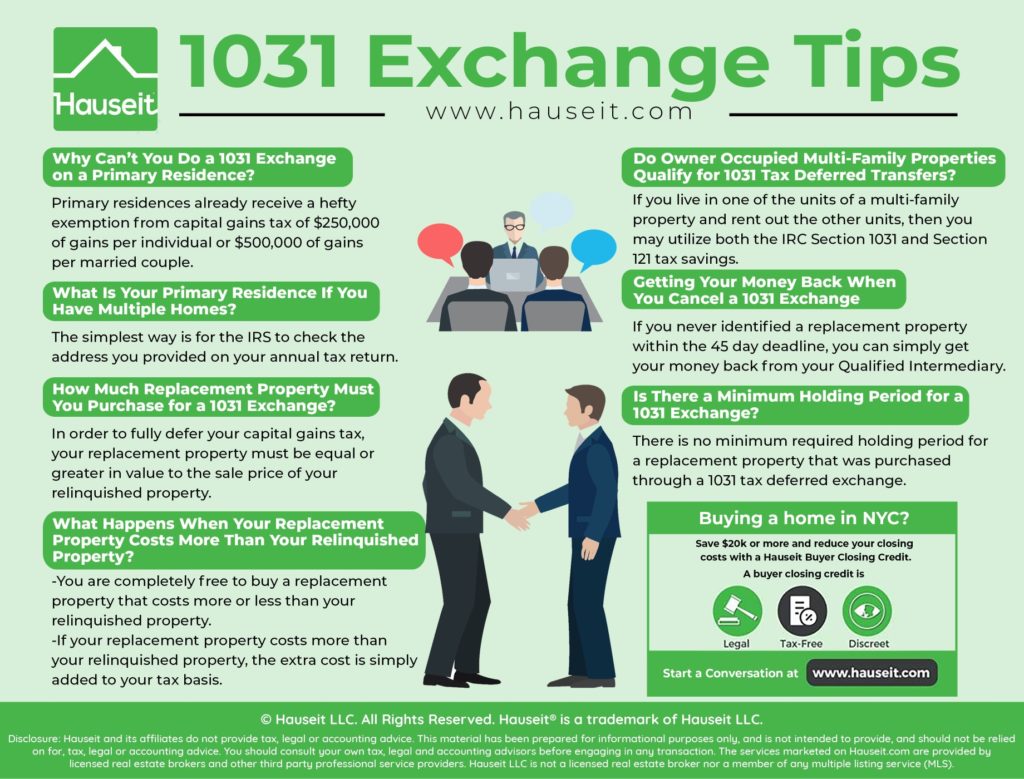

How To Do A 1031 Exchange In Nyc Hauseit New York City

Income Tax Deferral Strategies For Real Estate Investors Advisors To The Ultra Affluent Groco

Instructions For Form 1099 S 2020 Internal Revenue Service

Understanding Section 121 The Universal Exclusion On A Home Sale