Irs Code Section 72 M 7

3 10 72 Receiving Extracting And Sorting Internal Revenue Service

Instructions For Form 1040 Nr 2019 Internal Revenue Service

Internal Revenue Bulletin 2020 29 Internal Revenue Service

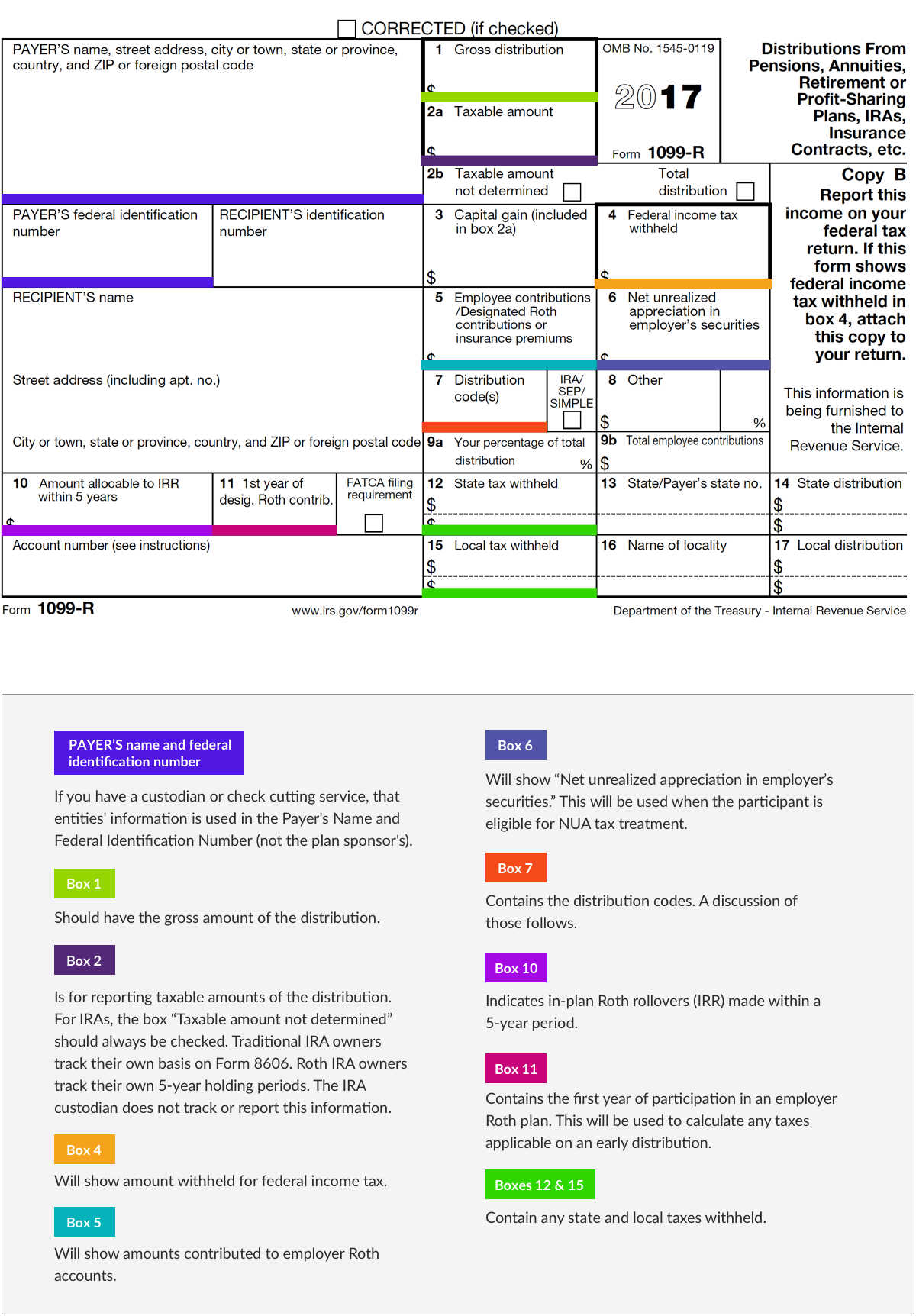

Form 1099 R Distribution Codes For Defined Contribution Plans Dwc

3 11 6 Data Processing Dp Tax Adjustments Internal Revenue Service

Secure Act Series Big Changes For Beneficiaries May Affect Your Financial Or Estate Plan

The regulations promulgated pursuant to the statutory authorization contained in section 72 m 7 provide that an individual will be considered to be disabled if he or she is unable to engage in any substantial gainful activity by reason of any medically determinable physical or mental impairment that can be expected to result in death or to.

Irs code section 72 m 7. Paragraph 2 a iv shall not apply to any amount paid from a trust described in section 401 a which is exempt from tax under section 501 a or from a contract described in section 72 e 5 d ii unless the series of payments begins after the employee separates from service. Any other distribution subject to an exception under section 72 q t u or v that is not required to be reported using code 1 3 or 4. 1 imposition of additional tax.

Generally the amounts an individual withdraws from an ira or retirement plan before reaching age 59 are called early or premature distributions. Paragraph 2 a iv shall not apply to any amount paid from a trust described in section 401 a which is exempt from tax under section 501 a or from a contract described in section 72 e 5 d ii unless the series of payments begins after the employee separates from service. If any taxpayer receives any amount from a qualified.

Most retirement plan distributions are subject to income tax and may be subject to an additional 10 tax. The irs defines disability for this purpose in irc 72 m 7 and the definition is quite strict. An individual shall be considered to be disabled if he is unable to engage in any substantial gainful activity by reason of any medically determinable physical or mental impairment which can be expected to result in death or to be of long continued and indefinite duration.

8 b d k or p. Irc 72 m 7 is just a section of the tax code that deals with pension distributions. 72 a 2 partial annuitization if any amount is received as an annuity for a period of 10 years or more or during one or more lives under any portion of an annuity endowment or life insurance contract i r c.

Use code 4 regardless of the age of the participant to indicate payment to a decedent s beneficiary including an estate or trust. This section has no bearing on the eitc other than defining what disability is. Certain proceeds of endowment and life insurance contracts t 10 percent additional tax on early distributions from qualified retirement plans.

The section you are referring to is intended to show one of the exceptions to the 10 excise tax assessed under 72 t. Internal revenue code section 72 t annuities. Irc section 72 m 7 and related regulations define a participant as disabled if he or she cannot engage in any substantial gainful activity because of a medically determined physical or mental impairment expected to result in death or to be of long continued or indefinite duration and can furnish proof of this condition in the form or manner required by the irs.

Withdraw Without Penalty

Irs Releases Clarifying Faqs On Cares Act Retirement Plan Relief

Https Www Raymondjames Com Media Rj Dotcom Files Wealth Management Why A Raymond James Advisor Client Resources Tax Reporting 2019retirementtaxpackagesguide Pdf

Https Hr Osu Edu Wp Content Uploads 403b Plan Doc Pdf

Https Dl Acm Org Doi Pdf 10 1145 3077136 3080840

Https Www Epinfrastructure Cz Wp Content Uploads Epif Ye 2018 Annual Report Pdf

Https Www Epinfrastructure Cz Wp Content Uploads Epif Annual Report 2019 En Pdf

Runoff Computations For Water Projects Proceedings Parts I And Ii Unesco Digital Library

Https Us Matthewsasia Com Resources Docs Pdf Literature Ira Application Current Pdf

Pin On Tax Time

72t Distributions The Ultimate Guide To Early Retirement Above The Canopy