Internal Revenue Code Section 482

Sec 482 Allocation Of Income And Deductions Among Taxpayers

Income Shifting Common Ownership Or Control Under Code 482 In An Inbound Transaction Lexology

Transfer Pricing Rules

20 1 5 Return Related Penalties Internal Revenue Service

4 46 4 Executing The Examination Internal Revenue Service

Https Www Jstor Org Stable 20771897

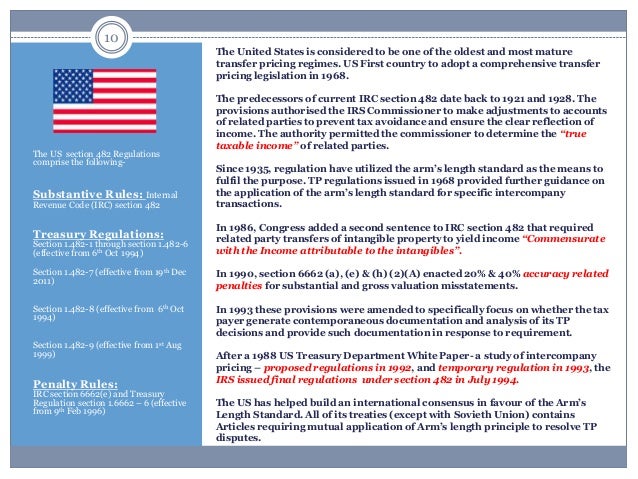

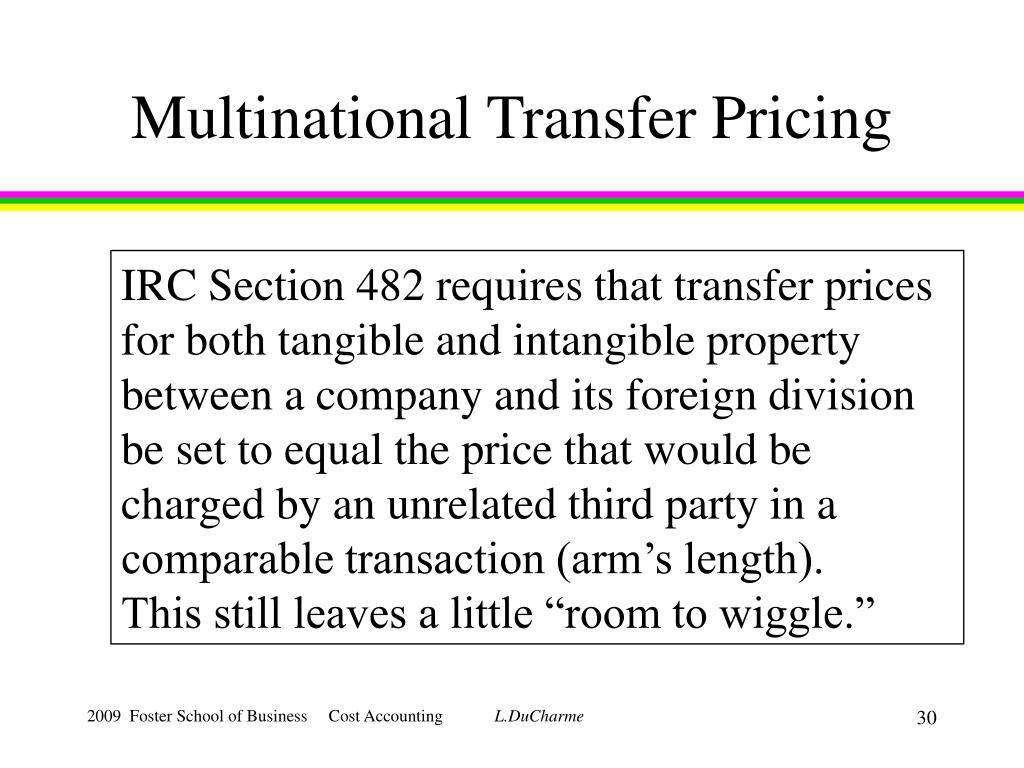

The purpose of section 482 is to ensure that taxpayers clearly reflect income attributable to controlled transactions and to prevent the avoidance of taxes with respect to such transactions.

Internal revenue code section 482. Internal revenue code 482. In any case of two or more organizations trades or businesses whether or not incorporated whether or not organized in the united states and whether or not affiliated owned or controlled directly or indirectly by the same interests the secretary may distribute apportion or allocate gross income deductions credits or allowances between or among such organizations trades or. Source credit amendments effective date regulations savings provision miscellaneous 482.

The study shall include a review of the contemporaneous documentation and penalty rules under section 6662 of the internal revenue code of 1986 a review of the regulatory and administrative guidance implementing the principles of section 482 of such code to transactions involving intangible property and services and to cost sharing arrangements and an examination of whether increased disclosure of cross border transactions should be required. For more detailed codes research information including annotations and citations please visit westlaw. Allocation of income and deductions among taxpayers.

Section 482 places a controlled taxpayer on a tax parity with an uncontrolled taxpayer by determining the true taxable income of the controlled taxpayer. From title 26 internal revenue code subtitle a income taxes chapter 1 normal taxes and surtaxes subchapter e accounting periods and methods of accounting part iii adjustments jump to.

Irs Faces Big Decisions 482 Transfer Pricing Rules

Introduction To Transfer Pricing

Overview Of Transfer Pricing Ppt Download

Http Hacienda Gobierno Pr Downloads Pdf Determinaciones 12 12 Pdf

Ppt Management Control Systems Transfer Pricing And Multinational Considerations Powerpoint Presentation Id 443803

Gale Academic Onefile Document Reactions To Schedule Utp How Companies Use Schedule Utp Can Provide The Irs With Insight Into The General Reporting Behavior Toward Uncertain Tax Positions

U S Docs And Master File Transfer Pricing Apples And Oranges Mantegani Tax Pllc

Https Www2 Deloitte Com Content Dam Deloitte Us Documents Tax Us Tax Inside Deloitte Global Business And States 20challenges To Taxable Income Pdf

How To Use Transfer Pricing To Protect Reit Income

Http Www Mtc Gov Uploadedfiles Multistate Tax Commission Uniformity Uniformity Committee And Subcommittees 2012 Winter Committee Meeting Mtc 20state 20use 20of 20irc 20section 20482 20authority Pdf

Https Www Jstor Org Stable 20767797

How The Irs Expects Taxpayers To Deal With Transfer Pricing

Https Www Irs Gov Pub Int Practice Units Iso9411 08 01 Pdf